Compound Annual Letter — 2018

Compound’s review of the market in 2018 + forward looking thoughts on 2019 as told to our investors

Below is a modified-for-confidentiality version of the annual letter we sent to our Compound Fund III investors.

Dear Compound III investors,

Over the course of 2018 we invested in 11 new companies, made 3 follow-on investments into existing portfolio companies, and invested in 11 new blockchain companies.

We also had 1 exit in Sayspring and 1 dissolution.

After an incredibly productive 2018, we’ve decided to reflect on our thoughts on the status of the markets we operate in, as well as the sectors we invest in looking forward to 2019.

Overall VC Market Conditions

In 2018, venture capital as an asset class saw the continued rise of mega funds, most notably Softbank’s $100B Vision Fund, in addition to multi-stage, $1B+ vehicles from the likes of other legacy venture capital funds. These massive funds have created somewhat of a kingmaking dynamic.

Most VC categories tend to be viewed as largely duopolistic at best (at least within a given continent). In areas where money can be traded at a moderately known rate for user acquisition, we’ve seen capital flowing at the first signs of product-market fit. The reason for this, we believe is 3-fold:

- As online ad networks and marketing platforms (like Facebook, Instagram, Youtube, Adwords) have become increasingly efficient (and thus marketing strategies have become somewhat commoditized) a disproportionate amount of spend has gone towards acquisition strategies. Some have even pegged that direct-to-consumer startups spend as much as 70% of their venture capital raised on marketing.

- Moreover, the abundance of larger funds has increased mid to late-stage prices, which then creates a need to deploy a significantly larger chunk of capital into your winners to maintain/increase ownership. Once companies (and investors) believe they’ve figured out the above mentioned user acquisition economics, venture capital is fuel to the fire, in its most pure form. And fuel prices are low. As a result, venture capital has moved further away from its intended purpose as risk capital.

- We’re clearly towards the end of an innovation cycle and a bull market cycle (more on this later). With liquidity windows only stretching out, we’re seeing older GPs raise larger funds, faster, in an effort to prepare for darker days, or possibly have one last decade of fees. As this bull market has stretched to historic lengths , we’re in what could be the last stages of heavy LP mega-fund appetite, something that these funds thought was 2–3 years ago, when they raised their last, smaller-but-still-massive fund.

All of these factors leads to a widespread belief that in certain categories capital is now a differentiator. Masa at Softbank made this point slyly when he threatened publicly to invest in Lyft, during Softbank’s Uber negotiation. We’ve seen this “capital as a differentiator” model play out in other categories with rounds raised for companies like Wag, Hims, Brandless, and more.

As a seed stage venture fund that invests against largely technical theses, we don’t believe the same existential threat holds in most of our categories and companies. Put more bluntly, Facebook and Google ads and the pricing efficiency of attention aren’t going to help our startups solve their problems. In companies creating deep technical IP, capital is not a differentiator, but is merely an enabler for hiring top talent and increasing the number of experiments that can be run in a given timeframe.

The seed market

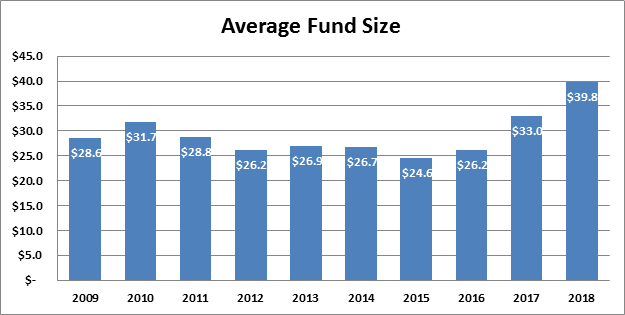

In 2018 we continued to see more new funds raised in the US (111 new first time US VC funds), as well as the average sub-$100M fund size continue to increase, creeping up to north of $39M.

We believe this happened for 2 reasons:

- With the rise of Micro-VCs back in 2014, we’re now starting to see more 2nd and 3rd funds from the first cohort of micro VCs.

- The Seed Phase has created a gap in the market, which funds are trying to solve with larger seed funds. Put simply, the bar to go from seed to series A has increased, resulting in more financing rounds (2.1) and more capital being raised pre-A (~$3.2M on average, $2.1M median).

Where does Compound fit in, in 2019?

Compound is a thesis-driven VC firm investing at inflection points of cutting edge technologies on the brink of commercialization.

When we set out to raise our third fund we intentionally sized the fund at $50M despite outsized investor demand. While we’ve seen many peers continue to drastically increase their fund sizes over the years, we still feel deeply convicted in our fund size decision. A $50M fund allows us to be a full-stack seed phase partner to founders, with the ability to lead pre-seed and seed rounds, while still being able to achieve our target ownership as co-leads in some instances.

Our pre-seed strategy allows us to invest in segments we feel don’t de-risk much from day 0 to Series A, such as robotics, computational biology, or consumer internet. Our seed strategy allows us to lead with independent conviction and act as strategic co-leads given our thesis-driven industry expertise In addition, as insiders, we can use our independent conviction to increase our ownership pre-series A.

Sectors we invested in

2018 saw us continue to dive deeper with our research, scale our networks, and make investments into core thesis areas including machine learning, robotics, blockchain, and healthcare (both digital health and computational biology), among others.

AI & Machine Learning

AI & machine learning continues to be a fundamental technology that we believe will proliferate to many segments moving forward. In 2018 we made investments in this category across ML-enabled creative tools, animation, and simulation/synthetic data (AI Reverie).

On a macro level, 2018 was another banner year for machine learning as we continued to see a breakneck pace of research being published. With that said, we think that the competitive environment for “AI-first” companies has become significantly more complex. We believe the market misjudged both the pace at which AI would improve, as well as the willingness by large companies to own horizontal types of machine learning at low-costs to the consumer. In addition, we believe many of the low-hanging fruit use-cases for deep learning were over-invested in in 2017/2018 and thus have picked specific categories to stay away from in the sector.

All of this has pushed us towards a few key beliefs with respect to investing in AI-first companies moving forward:

- Companies building on the basis of being “state of the art” today will need more than technology to win markets.

- There is an opportunity in being an expert at adopting the bleeding edge of AI research into a commercialization and productization plan.

- Companies must either be bleeding edge with an applied focus, very narrow with a long-term data advantage, or a pickaxe, as anything in-between these feels commoditized.

Moving forward in 2019, we’re specifically interested in applications related to unsupervised learning and reinforcement learning. In addition, we believe continued advancements in research, as well as more data points on proper paths for commercializing research will enable multiple founders to build companies in our thesis areas.

Robotics

Compound invested in three robotics companies in 2018 including leading or co-leading rounds for (ARobotics and BRobotics) as well as a small investment into (CRobotics).

Multiple macro factors continue to impact our excitement for robotics including falling component costs, better intelligence, a continually increasing willingness on the customer end to utilize automation, and related, labor issues across multiple industries.

Our view on investing in robotics companies continues to highly prioritize what we call “full-stack” companies, which utilize their proprietary-built automation (robot) in order to achieve economic or product efficiencies that their competitors cannot. (ARobotics) fits this thesis as a full-stack food provider utilizing automation to drastically increase the economics of food service.

If robotics companies must deal with a B2B2C client arrangement, we believe that selling a robot to an end-user is not the correct business model but instead abstracting away the “how is this done” (i.e. a robot) and focusing on the “what is done” (i.e. providing a better service) is the correct approach. This has been referred to by some as “robot as a service”. (CRobotics) does this for synthetic biology companies.

While both full-stack and RaaS companies can create great unit-economic businesses, we do believe that the market is massively mispricing the upside of applied narrow robotics use-cases, and believe that similar to many venture categories, large robotics companies will land and expand horizontally into new sectors or use-cases vs. a future of fragmented market leaders across each individual type of service.

Lastly, we still believe there is core infrastructure that needs to be built in order to enable our robot-heavy future. Companies like (BRobotics) are enabling this future.

In 2019 we continue to look for full-stack robotics companies as well as core infrastructure as exciting areas to invest in within robotics.

Blockchain

This past year, Compound made a number of investments in the blockchain sector and established deep thought leadership. Many of these were protocols such as Livepeer (live streaming protocol), Computable (decentralized data marketplace), Graph (data querying protocol), and Redacted (verified computation for blockchain scalability), amongst others. In addition, Compound co-led Casa’s seed round along with Lerer Hippeau Ventures. Casa is a personal key system for blockchain custody and key management.

The hype and excitement we saw in the blockchain sector beginning in late 2016 was stopped in its tracks beginning in early 2018 as public cryptocurrency prices quickly headed on a downward trajectory, the likes of which has forced teams to hunker down and focus on their go to market strategies and business models in preparation for a prolonged “winter”. This wasn’t unexpected, as Josh wrote in May of 2017:

It hasn’t really mattered what the actual project is or if there are any users at the time, as the token prices are soaring on the dates of these ICO’s. So long as they had the word “Internet” in their business model, companies in the 90’s would go public and see their market caps soar despite the state of the actual business at the time as well. As investors see soaring prices, the fear of missing out takes hold so they too buy these tokens, which in turn drives other investors who don’t want to miss out to do the same, further driving up the prices. As the old adage goes however, “history doesn’t repeat itself but it does rhyme”. We know from history that these virtuous cycles don’t last forever and eventually bubbles have to pop.

While the media often writes obituaries for the space at large, we view this rapid shift in sentiment as positive; forcing companies and projects to build sustainable business models and move at rapid paces instead of keying in on vanity metrics. Furthermore, the over-investment in solving difficult technical problems, brought a significant amount of talent into the space, laying the groundwork for the development of a technological system without the same flaws that have been apparent for a number of years now.

We remain excited about the possibilities here and believe that akin to several other periods of bearish sentiment as it relates to startups over the past 20 years, enduring companies will be started during this time. We’re most excited about teams solving for known weaknesses with public blockchains (privacy, scalability, etc) and applications built atop that infrastructure where the idea of “programmable value” is the core value proposition.

Healthcare

We remain very excited about the healthcare space broadly and continue to actively invest in both the digital health and computational biology sectors. These investments included pre-seed investments in (redacted) and Lune, as well as seed round investments in Juvena and Boost Biomes.

While we’ve been investing in the digital health sector at-large for a number of years, there are several factors that have been driving our increased interest in computational biology. Specifically, the cost of sequencing the human genome and the microbiome continues to fall (as seen above). This has led to a massive increase in the amount of data becoming available, which when combined with Moore’s Law and the falling cost of cloud compute creates a massive opportunity for the use of machine learning to generate insights.

While certainly distinct from traditional digital health investments, there’s more and more overlap between AI/ML software companies and computational biology companies. We understand that in most instances, these investments can take longer than your traditional digital health startup but the potential outcomes can be extraordinarily larger as well. Given this dynamic, we’re comfortable owning a little less of these companies than average and are comfortable participating in rounds in addition to leading or co-leading.

Looking towards 2019

Macroeconomic volatility

The effects of public financial market volatility and its impact on seed investing, is unclear to us. Macroeconomic volatility could mean a tightening of downstream capital, which we are preparing our founders for and are positioned to take advantage of with our reserves to support our promising companies. Ultimately we are investing in what we believe to be companies that will withstand market cycles and build up towards immense value creation over a 7–10 year time horizon, not 1–3.

In terms of the exit market, we feel that based on the diversity of acquirers for tech companies today, the healthy balance sheets of many larger players, and the existential threat that technical inflection points breed, our portfolio specifically could have a higher ability to drive premium acquisitions in a down market vs. other more consumer-spend focused startups may.

With all of this said, some of the generational startups of our last innovation cycle were started in the ashes of a financial downturn and thus if market volatility does hit, we expect to remain aggressive while being continually disciplined with ownership metrics and managing portfolio company burn rates.

Investing & Fund Management

We expect 2019 to be a big year for Compound III as we deploy the last of our capital earmarked for initial investments and begin to see maturation across the entire portfolio.

For new investments, we have multiple theses we continue to build out, iterate upon, and source potential opportunities for. These span existing categories as well as new ones including family planning, space, spatial computing, digital identity, and more.

For existing investments, we continue to support our portfolio with the help of our new Head of Platform, Nicole Imhof. As a team we will continue to help our founders build out elite technical teams, execute on commercialization of new technologies, and leverage our network for various company-specific needs. On the financing front, we project multiple companies will raise follow-on capital this year, which we are excited to utilize our ample reserves to maintain and increase ownership in core positions for.

In conclusion, we continue to feel grateful to have you all on our side as investors and advisors and are looking forward to spending more time with you all in 2019. If you’d like to dive deeper into any part of this letter, please don’t hesitate to reach out.

Regards,

Compound Team