Below is our slightly edited for confidentiality 2019 annual letter to our investors.

Dear Compound I investors,

In 2019 we invested in 4 new companies, followed-on into 11 existing companies, and saw 2 companies exit. In total we deployed $xM into new investments, $xM into existing investments, and saw proceeds of ~$xM due to exits from Indio and Clear Genetics.

In total the fund has now invested $xM of the ~$50M of committed capital into x companies, and called $xM, with an MOC of ~x.

We’re excited to share with you our annual letter surrounding our portfolio, views on the market, and the evolution of some of our thesis areas moving forward.

Our Portfolio

As we predicted in our initial model, in 2019 (year 3) our portfolio has matured where we’ve begun to meaningfully follow-on into companies we invested in at the pre-seed/seed stage. Our largest follow-on investments were into Indio’s Series B led by Menlo Ventures and 8VC, Wayve’s $20M Series A led by Eclipse, Unannounced’s $xxM Series A led by VC, xx’s Seed led by VC, and Osaro’s $16M Series B led by King River Capital.

Our core job as fund managers is to not only build partnerships with founders early on via initial investments, but also to make sure that we continue to deploy larger sums of capital into our most promising companies. We feel strongly that we did that well in 2019, and thus were able to defend ownership, increase capital allocated to potential fund-returning companies, and support companies in need of some more maturity ahead of a value inflection point.

While many firms consistently take the view that if a certain tier of investor is leading a next round, a firm should do their full pro-rata, increasingly we’ve felt that at the early-stages signal has deteriorated as “Series A” firms have become full-stack firms and the Series A in some ways becomes call-options for long-term, multi-year capital deployment. Because of this, despite some data suggesting historically it was dominant to always follow with full-pro rata with certain tier funds, we’ve been increasingly focused on making sure our follow-on process and check size is modeled surrounding our internal beliefs of inflection points of the businesses. At times this means buying up above pro rata to increase ownership (increasingly not possible) and at times not filling full pro-rata and taking some dilution.

In terms of new investments, you’ll notice we were slower to deploy capital this year and expect that we will be investing Compound I throughout the majority of 2020, with a little over $xM earmarked for new investments and $xM for follow-on in the remainder of the fund. Our new investments in 2019 included Pre-Seed investments in Guesser, ML Infrastructure Company A, and Company B, as well as a small investment in (embryo synthesis company).

The seed venture landscape has largely complained about full-stack funds coming down into seed and out-pricing them by writing call-options for later rounds. While that does happen from time to time, in our experience this year, that was not the case. One may look at our slower pace and lack of investable opportunities in our eyes in 2019 as a result of lower quality or volume of deal flow. We don’t believe this was the case as volume in 2019 did not dip versus prior years (however this is always top of mind for any smart investor). With all of this said, we continue to feel good about our process for finding founders early, in addition to our growing brand, network, and distribution within the ecosystems we care about.

As you know, we tend to take a very research-heavy and thesis-driven approach to investing in startups. We find categories that we believe will drive outsized venture returns over the next 10–15 years that we feel uniquely suited to invest in, build views on what types of businesses we’d like to back, and let founders either fit within or shatter those views (equally as strong signal to both). Often our portfolio companies are built on the premise of a technical shift or innovation that is either a macro trend or an in-house development that then enables them to be uniquely suited to build, scale, and defend a product/business model in a duopolistic and venture-scale way.

Part of our strategy is to be intentionally early to categories that we feel are weakly understood and underinvested, build out core theses and investments in these categories, and then continue to utilize our domain expertise and emerging brand in these categories to reap venture returns across multiple funds. Our hypothesis for 2019’s pace is that many of the categories we focus on were in various flux points with their development and penetration that caused us to either feel there were fewer venture-scale investment opportunities, founders, or companies. We will go into this more in-depth shortly.

While we recognize the importance of deploying capital and the impact on IRR slower deployment can have, when investing on a 10 year time horizon, we don’t feel it’s wise to lower the bar or over deploy in order to raise our next fund in an attempt to time the market. Fund investment periods have gone from 5 years to 3 years and now in some cases to 18 months, and we feel this is bad for both LPs and VCs in terms of diversity of both time and ecosystem development across a portfolio like ours.

Exits

In 2019, two of our portfolio companies, Indio and Clear Genetics, were acquired for a combined x return and over $xxM in proceeds.

Clear Genetics, a software and chatbot developer for genetic counseling that was acquired by Invitae, was a company that we backed just before YC Demo Day in 2017. The company was able to build early distribution and great core technology. (Removed commentary on distribution, sales cycle, and M&A process.)

Indio, a small business insurance software company that was acquired by Applied Systems, was a company that we backed at their seed round in 2016. Indio is an example of a company that was growing incredibly quickly, had great success fundraising, and had consistently turned down acquisition offers as their product commercialization had begun to scale. (Removed commentary on M&A process, business metrics, and outcome.)

We had multiple core learnings and observations from our reflections on these exits and others within our ecosystems of focus.

First, it is clear to us there is meaningful value creation that can come from building core technological IP, that allows great optionality in downside commercialization processes. We have seen this previously in this fund in Company Name (acquired by XX) in addition to Company and others, with these companies being slightly slower towards commercial adoption but leading to x.x+ outcomes and $xxM+ offers each time.

The second learning is the increasing understanding by cash rich incumbents surrounding M&A’s value. Mike previously wrote about this dynamic of startups having to be too early in order to disrupt large tech platforms (and some of the resulting acquisitions). This behavior on the M&A side has now far expanded outside of just the core tech platforms that have been so incredible at both additive and defensive M&A over the past 5–8 years and into incumbents that realize all companies must become technology companies (sorry for the cliche).

The third related learning has been around scale and founder incentives. As becoming a founder has become more en vogue over the past decade (and VCs have followed a similar trend) we’ve started to pay attention more to vetting the scale of ambitions for our founding teams. Our view is that with the proliferation of “founder as a career”, we may have lost some of the (frankly) irrationality that comes with starting a company with the goal of building a massive, venture-scale outcome. Consequently, we are continually focused on both vetting the scale at which founders truly want to build their business, as well as the opportunities to make sure we can perhaps alleviate early economic concern via secondary (Removed commentary on examples where we have done this or this has happened in portfolio).

Dissolutions

We had 2 dissolutions in our portfolio this year, both pre-seed investments, in A and B.

A, (company description), fell victim to many of the things we will go into below surrounding poor understanding of customer acquisition costs in healthcare, paired with an inability to provide enough value for a high-priced product.

B, (company description) unfortunately wasn’t able to validate some of its early technical milestones in order to raise follow-on institutional capital. We ultimately recognized this as a risk and misjudged how the follow-on financing market would view this particular founder, who did not come directly from industry, as backable.

These dissolutions resulted in a combined loss of $600k bringing the total dissolutions in the fund to $1.6M.

State of the Market

A year ago we wrote about what we called capital as a differentiator and a potential kingmaking effect that was arising due to Softbank’s Vision Fund, a broader increase in mega-funds, and businesses heavily built around scaling paid customer acquisition. We walked through case studies of companies such as Hims, Brandless, and Wag at last year’s AGM and showed material negative performance in many of those companies this year. See below for one of the updated slides from this year’s AGM.

While our initial view that Softbank and other VCs were attempting to kingmake certain categories, we believe that these large investors may have underestimated the depth of the private capital markets, and the size of the universe of investors that were willing to come into similarly early rounds, and over capitalize companies in competitive spaces. Thus capital went from a differentiator, to mostly a dilution mechanism, as well as a fuel for incredibly inefficient customer acquisition or scaling business economics.

The latter speaks a bit to us then seeing what we call capital as a disaster (CaaD). CaaD is/was the result of an influx of larger funds, leading to larger rounds, resulting in larger expectations, all ahead of meaningful value inflection points, business-market fit, or company readiness, leading to larger problems. The poster child for CaaD in 2019 was obviously WeWork, which saw over $35B of enterprise value destroyed in weeks ahead of its IPO.

The various CaaD scenarios eroded value in both private and public markets, as companies that hadn’t achieved what some perceived as dominate position within their given vertical or category suffered at their IPOs.

Despite some of the doom and gloom we’ve talked about related to larger funds, larger rounds, and everything that comes along with that, we actually think that this behavior is here to stay in 2020.

While the industry can opine about how profits are back en vogue and unit economics are being more closely studied, across all of tech (and especially in areas like SaaS or fintech that are well-understood and have had recent liquid success) there is still a ton of dry powder sitting on the sidelines looking for places to park their capital. Over 15 $500M+ VC funds closed over $14B in capital in 2019, and there were another 25 open funds targeting $500M+ as of September 2019.

This capital needs to be deployed and whether these funds view themselves as series A, B, or growth stage investors is irrelevant as they will aggressively compete for a largely known universe of deals across stages in areas where they see large upside and ability to deploy large sums of capital over multiple rounds.

While we’ve talked a lot about late-stage growth investing and overcapitalization of companies, we generally remain incredibly bullish on private markets and venture-scale value creation more than ever before, with billion dollar exits up on average over 7x from a decade prior. Private markets will continue to eat up a larger chunk of returns versus publics, as the IPOs of yesterday are now growth rounds of today, and some of the mega funds we’ve discussed could reap those rewards.

Sectors

As we’ve mentioned in the past, we have a few core sectors which we feel encompass around 3/4ths of the investments we will make out of Compound I. When we categorize companies and sectors, they often begin to blend as industries mature and companies perhaps increase their scope with maturity. Over the year each of these sectors has matured or had unique developments that we’ll go through now.

Machine Learning

In 2019 we led ML Infrastructure Company’s Pre-Seed round, and followed on into Wayve’s Series A round and Stealth Seed round.

Last year we established a few of our core beliefs surrounding investing in machine learning companies. One of the core takeaways we had was that as machine learning has matured, we are only more deeply convicted that competing on the “best algorithm” will not create meaningful long-term value.

In addition, we also stated that we believed that the low-hanging fruit use-cases for deep learning were over-invested in from 2016–2018. We believe that as the large platforms have pushed down the cost of core use-cases surrounding deep learning and built more core infrastructure and applications into their cloud platforms, a sea of ML startups have struggled and won’t be raising additional capital.

Our gut tells us that this low-hanging fruit eradication, steeper competition for the large tech platforms, and disappointing startup outcomes, led to a bit of pullback on applied machine learning companies in 2019 at the seed stage. We continued to see tons of investment in the developer tooling and infrastructure layer, which led to our investment in ML Infrastructure Company, but increasingly it feels as if founders are more deeply validating the axis of competition and true defensibility for applied ML companies in today’s market.

Despite this short-term reset, the machine learning industry continues to evolve at a breakneck pace, as state of the art is disrupted across various use-cases seemingly quarterly, and large organizations are pushing the boundaries on both compute and data scale utilization.

With this in mind, we are still intrigued by founders crossing the chasm between research and commercialization in newer frontiers of machine learning across a variety of industries, as well as fully vertically-integrated companies that build internal tooling to create efficiencies while providing a core value-prop to customers (similar to full-stack robotics companies).

With more traditional and deeply penetrated ML techniques, we’re still excited about ML applied to areas such as healthcare, where larger platforms will come under data privacy scrutiny (as Deepmind did) and startups can amass datasets that create a semblance of a moat. In addition, we believe that technologies like machine learning and computer vision will continue to be core components to building some compelling products in consumer-facing applications as existing companies compete away traditional consumer experiences via owned distribution.

Robotics

In 2019 we built meaningful positions by following-on into Osaro’s $15M Series B, and Ono Food Co’s Seed. We did not make any new robotics investments.

At an industry level we remain excited about the economic and technological shifts (such as increased willingness to spend on robotics and continual falling hardware costs) related to automation as well as certain layers of intelligence and infrastructure that exist at the intersection of hardware and software. Our view on robotics companies continues to be investing in full-stack companies that can capture the value they create with automation, while maintaining the flexibility to roll out their products in a staged way and even at times blending human and machine labor to provide value to their end customers.

We increasingly favor these types of companies in funding environments where we’ve seen multiple well-funded seed companies go out for Series As with pilots, be unable to convert to heavily recurring paid contracts with a potentially risk-averse customer, and then go back to the market for seed extension rounds.

While we are built as a fund to support our companies through these rounds, they ultimately are very difficult for robotics companies as they take deeper dilution, often don’t get enough capital into the company to meaningfully progress on R&D, and at times can raise the bar for a Series A that will need stronger numbers once there is a small amount of customer data. In addition, the install base of investors willing to back robotics companies has not materially grown over the past 18 months or so.

Moving forward in 2020 we’re excited to continue to look for full-stack robotics companies that are targeting areas largely outside of the warehouse and construction industries as we feel the competitive dynamics and/or customer dynamics for new entrants makes these areas difficult to invest in at the pre-seed/seed stage today.

Healthcare & Bio

In 2019 we followed-on into HealthA $15M Series A, Seed+ rounds for HealthB, HealthC, and HealthD, and made a small new investment in a stealth embryo synthesis startup called XX.

Our investments and active theses in healthcare continue to be a core area of focus for us at Compound. We’re willing to invest across the entire spectrum of healthcare/bio which we believe starts at digital health, goes through computational biology, and ends at companies that would be more classically categorized as Biotech.

Over the course of the fund’s history we’ve made multiple investments in digital health companies across high world and economic value spaces such as mental health, women’s health, addiction treatment, and genetic counseling. With the rise of better hardware and software infrastructure surrounding quantified self and personalized medicine, we’ve seen a slew of new companies start in a variety of other spaces all going after consumer spend (and often with an eventual payer-centric model as well).

While we remain excited by many digital health companies, the problem that we’ve seen is one that is very similar to other consumer businesses we mentioned above surrounding capital as a differentiator; costly acquisition. While the first major wave of digital health companies performed quite well, just as D2C companies did, we believe a larger number of new entrants have shown weaker utility and marginal science, without a differentiated (and significantly more costly) customer acquisition strategy, while having a monetization path that often under-appreciates churn in these products (thus throwing off the CAC/LTV assumptions post-launch). As we’ve seen with Talkspace in our second fund, we believe it can be a great strategy to go B2C to build brand and customer loyalty, but only if the service value (and price point) is quite high, and even then we assume massive scale more easily comes from B2B distribution.

Another trend we’ve seen within healthcare has been the (supposed) blending of physical healthcare with digital experiences and tooling. Our investment in Tia, which we remain incredibly bullish on, is a good example of this. We believe that companies in this space must deeply understand where core spend comes from the patient, both on the reimbursable side as well as out of pocket, and must have multi-stage plans for understanding how the economics, NPS, and LTV are better than historical, traditional clinics. In addition, we like to understand how these businesses can become venture scale either with partners, by introducing a true digital moat, or again, with scaled B2B contracts.

Instead what we increasingly see is an optimization of a premium experience (which helps economics due to the membership fee), NPS (due to less pressure on the care team, which is subsidized by membership), and brand (which we feel is a weak moat from seed to series B, but helps acquire users in Tier 1 cities and can drive down early CAC).

To their credit, these are all understandings that our portfolio company Tia has pushed on from the beginning, increasingly pushing off the idea that they are purely an instagram wrapper around women’s health, but instead telling a story of a differentiated care model (both clinically and by reducing the cost of care via tech-enabled team based staffing), layering in highly profitable, out of pocket expenses, and building partnerships that can introduce large, nationwide scale quite quickly and capital efficiently to the business.

We’d love to find more companies like Tia that surround our various healthcare theses.

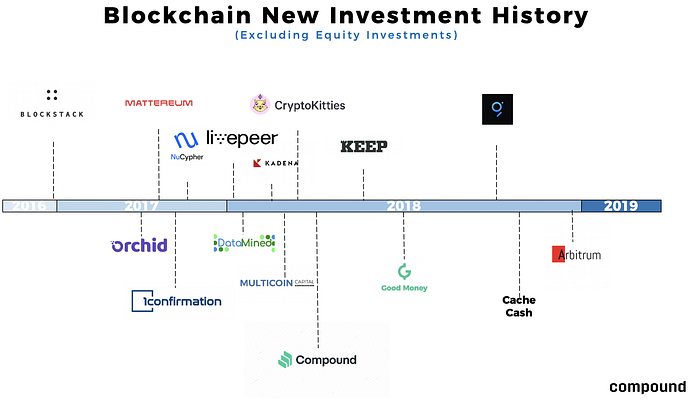

Blockchain

In 2019 we invested in Guesser’s Pre-Seed round, and followed on into LivePeer’s $8M Series A round as well as BlockchainA’s Series A round.

Our new investment activity has slowed considerably, a result of concurrent forces which we anticipated. Public blockchain technology is not yet ready for primetime for most consumer-facing use cases. As a result, while we’ve seen considerable growth in usage for certain applications (like Compound portfolio company, also called Compound, which raised a $25M Series A from a16z Crypto this year), the number of use cases is limited by the technical drawbacks. Relatedly, many of our investments are at the protocol layer and in some cases teams are building both the protocol and the application that sits atop.

Developing public blockchain protocols is a prolonged and arduous process compared to typical software application development. This is a result of the fact that it’s open-source and very difficult to update once deployed so a traditional “MVP” product isn’t possible in the same way that it is for most startups. This is further complicated by the fact that there’s monetary value that can be stolen from users in the case of any security flaws that can not be recovered so the traditional “move fast and break things” approach does not apply.

We’ve been careful to date in the size of our investments, deploying a total of $xM into blockchain projects in this fund. While we remain optimistic about the future of public blockchain technology, the market timing is still an open question that we hope we’ll gain further clarity on in 2020 and in subsequent years.

2020 and beyond

As mentioned above, our main goal for 2020 is to finish building the initial portfolio for Compound I (Fund 3) and continue to support our companies with follow-on capital. We currently have $xM left to invest in the fund which we believe will be ~8 more new companies and a strong reserve of capital for follow-ons, ending at about a 1–1 capital allocation ratio between initial and follow-on.

Projecting forward to 2020 initiatives and goals, we have a few key areas we’re focusing on surrounding the fund and its operations.

Hiring

On the hiring and team front, we expect to add 1–2 new team members this year (1 partner and 1 junior investor) in either SF or NYC. We are currently in the process with both of these. In addition, we intend to continue to add to our Venture Partners, while also announcing some new advisors over the next few quarters that more deeply reflect our core focus on emerging technologies and helping companies figure out commercialization and building engineering teams in the post-science project phase.

Incubation

On the fund front, we continue to believe that incubation is something we will move forward with on a cadence of every 12–18 months. Our filter for incubation vs. investment is viewed as one where our research has led us towards a very specific view on a certain type of company, product, and go to market we want to see executed upon, and that we feel we can and should spend meaningful time both as co-founders to the company as well as the first investors. We have killed multiple incubation processes as we dove deeper with key people, later realizing we weren’t best suited to be true co-founders in the business.

From there we aim to find a founding team to build the company with, finance the team, and remain heavily involved operationally for the first 12–18 months, in exchange for a small amount of common stock on top of preferred stock from our investment. At this point we plan to raise outside capital. As you remember, (removed context on prior incubations).

We currently are in the early stages of an incubation in (removed context and thesis) and hope to have more updates in 2020.

2020 Market

On the broader market front we’ve received many questions surrounding both public market volatility as well as private market corrections due to some of the distressed investments from the Softbank Vision Fund and a perceived chatter around profitability at the growth stages

As always with public markets, we aren’t going to pretend to have a strong view on when the pullback we’ve all waited years for will occur (some of our LPs likely do :) ). As mentioned, we continually believe that private markets are going to capture returns, and that public markets have just begun to understand the order of magnitude, value creation, scale, and pace at which some technology companies can grow, and that makes us comfortable.

Ultimately, we’re investing on a 6–10 year time horizon for this fund, and on that time horizon we are betting on various versions of the future that we believe in, hoping just 1 to 3 of those core companies have scaled impact on those futures. Because of this we don’t time the market with our investment pacing, or our fundraise cycle and instead build portfolios that we think will endure and build massive, defensible businesses over the following decade. It is our hope that our investors understand this and continue to believe in the growth and value of early-stage private market exposure in their portfolios, regardless of any minor changes due to denominator effects or broader public market pullbacks. That said, as a small, $50M fund, follow-on financing is an existential risk to nearly every one of our companies, and thus we feel one of our core jobs is to intimately and continually understand the depth and readiness of the follow-on financing ecosystems across every sector we invest in.

On the private market side, yes, investors continually are voicing concern about cash flow at the later stages in a post-WeWork world (as mentioned above). But again, we don’t feel we have seen any material impact on how Seed or Series A capital is operating. It’s our belief that Series B is the most difficult round to raise for vc-backed companies today, specifically in emerging and deep tech areas that we invest in. That said, the large amounts of dry powder, the increasing number of investors willing to take large bets on deep tech as these ecosystems mature, and the core IP being built within our companies, makes us feel comfortable that a perceived hunger for profitability and clear operating metrics will not force our companies into unfavorable or unrealistic dynamics that will impact the upside value of the business.

An additional point to make is that, historically in unique situations, we have sold portions or entire positions at the series D+ stages, largely selling into new investors or secondary buyers. We feel this opportunity has only become more prevalent and easy for us over the past few years as more investors have moved to late-stage private markets.

Compound as an enduring firm

With all of this commentary on the market, our approach, and the types of companies we like to partner with, we remain incredibly excited about the future of Compound. We feel that we’ve spent our first Compound fund building a strong portfolio and brand that optimizes for deep industry knowledge, a bottoms up thesis-driven view on the world, and high EQ and empathy for the founder journey.

We believe 2020 will be largely about scaling these early proof points in a meaningful way both in terms of team size, reach within the communities we care about, and more. As always, well done is better than well said, and we look forward to proving that this year and for many more to come.

Thank you for your continued belief and support.

The Compound Team